The Most Undervalued Artificial Intelligence Stock in the World

Baidu (BIDU:US is the largest search engine in China with over 80% search revenue share. Although many argue that search engine is dead, especially in China, with other internet giants and mobile app unicorn blocking search engine crawlers from collecting mobile app metadata, it’s undoubtedly search engine is an invaluable asset that can never be replaced.

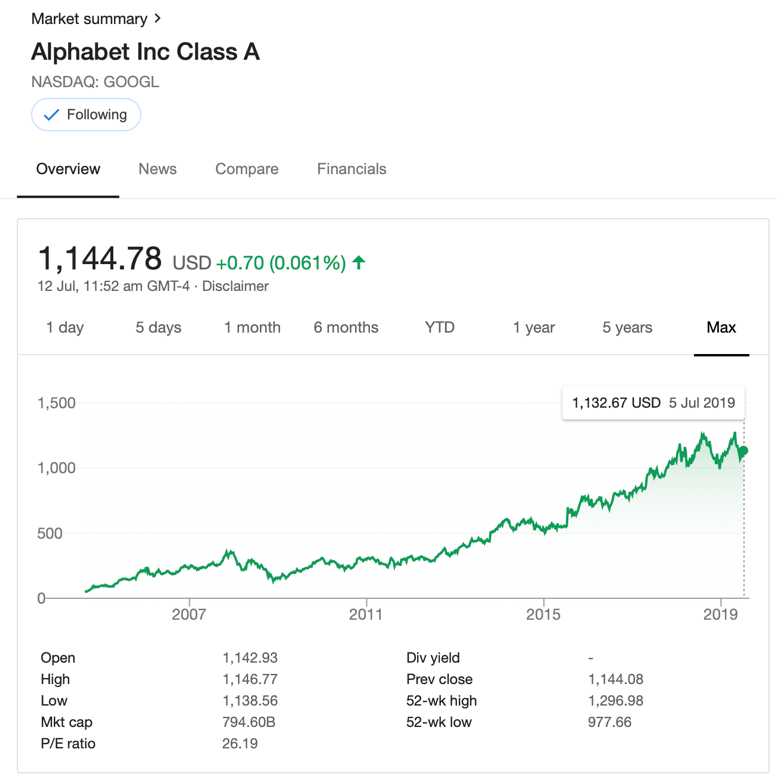

Same argument was being applied to Google GOOG:US (now Alphabet Inc) some years ago. Guess what. Alphabet Inc share price has been going up one straight line and it is worth US$794.6bn!!

Baidu, on the other hand, is only worth slightly under US$40bn. If you put Baidu and Alphabet in comparison, Baidu’s market capitalization is only a paltry 5% of Alphabet. If you compare the Real GDP of U.S. and China, China is only maybe 5-10% below U.S. But, China’s population is more than 4x of the U.S. In any case, why should Baidu market value be significantly lower than Alphabet Inc.?

Let’s take a quick look at Baidu’s businesses

Various Investments

- 58% in iQiyi – China largest online video streaming platform.

- Market cap – US$14.3bnValue of Baidu’s stake – US$8.3bn

- 20% in Ctrip – China’s largest Online Travelling Agent (OTA) with 80% market share.

- Market cap – US$20.62bnValue of Baidu’s stake – US$4.0bn

- Net Cash on balance sheet – over US$10bn and free cash flow is still growing at about US$3-4bn a year.

- In 2-year times, Net cash on balance sheet will swell to at least US$15-16bn

- Search Engine – The Abandoned, Unloved Child

- Generating RMB 23bn Free Cash Flow in FY2018.

- 20x P/E on FY2018 FCF translates to RMB 460bn valuation; or roughly US$66.7bn (@USDCNY 6.90).

Sum-of-the-Parts Valuation

- iQiyi – US$8.3bn

- Ctrip – US$4.0bn

- Net Cash by FY2021 – US$15bn

- China Search Engine – US$66.7bn

- Monopoly in China Autonomous Driving (driverless car) – US$40bn.

- Tesla’s market value is US$42bn and the company doesn’t have good safety track record. At best an ADAS level 3 technology which is far behind Waymo and Baidu.

- Artificial Intelligence – US$??bn

- No one knows what A.I. can do in the future, impossible to value Baidu’s leading A.I. technology in China.

- With trade war spat, Baidu’s A.I. will only be more valuable, regardless of the outcome.

Baidu’s Intrinsic Value = 8.3 + 4.0 + 15 + 66.7

= US$94bn + A.I. Tech Free of Charge!!!

Significant Share Buyback Program

Since Oct-2015, Baidu has announced a series of share buy program with minimum amount of US$1bn. Based on the company latest announcement post-1Q19 earnings call, Baidu had already announced a total of US$5bn share buyback program in less than 4 years!!!

Despite Baidu management guided low double digits revenue growth for 2Q19, and most likely for the rest of 2019, investors continue to hate this stock and the share price has gone back to 2013 level.

We believe that

(1) US$5bn share buyback program;

(2) old timer market darling to abandon child sounds a BIG BIG value alarm for value investor.

Yes, China economy may not do well this year due to trade dispute. However, it’s hard to imagine Baidu’s free cash flow to significantly decline from US$3.4bn in FY2018 to, let’s say US$2bn. Not to mention that Baidu had already spent RMB 56bn in R&D expenditures since its IPO back in 2005.

Imagine Baidu will generate the same amount of FCF, US$3.4bn, the stock is trading at 11.7x forward Free Cash Flow!!! We have never seen such a cheap internet giant in our life!!!

Just do a quick screening on HKEX and NASDAQ China internet industry. There are many companies are still burning through IPO investors’ capital while the stocks are trading at Price-to-Imagination; because there is no earnings or positive free cash flow to measure it!!!